Virginia Heyburn

Virginia Heyburn

1 min read

Financial Literacy Just Went Viral

Key Takeaways from This Blog:

1 min read

Key Takeaways from This Blog:

1 min read

Google, Mastercard, PayPal, American Express, and Coinbase quietly changed the script last week. They rolled out theAgent Payments Protocol, which...

1 min read

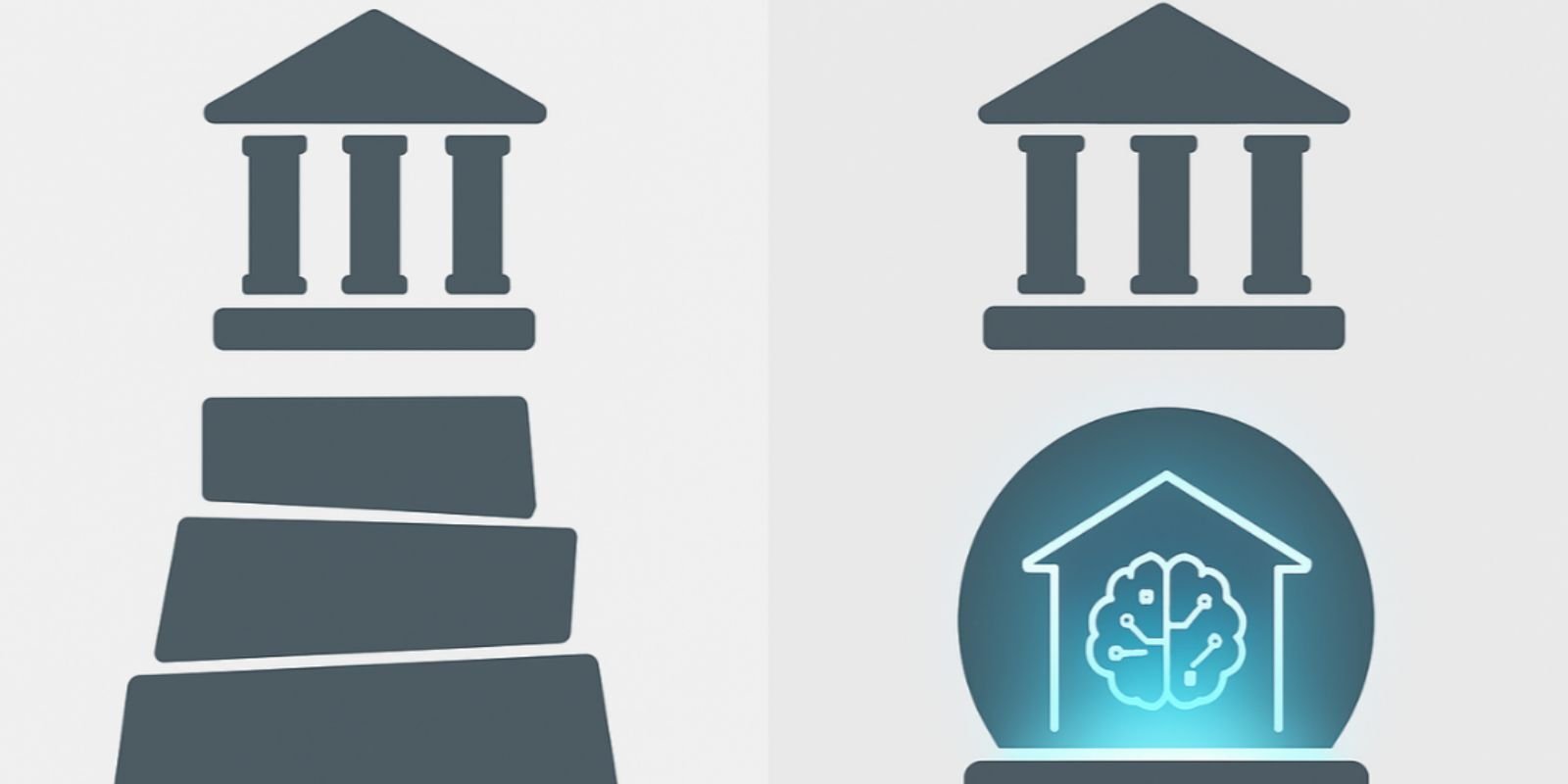

Financial institutions keep talking about "adding AI" to their operations. Installing chatbots. Deploying fraud detection models. Automating...