Fabio Biasella

Fabio Biasella

1 min read

Deposit Modernization Starts With Behavior, Not Products

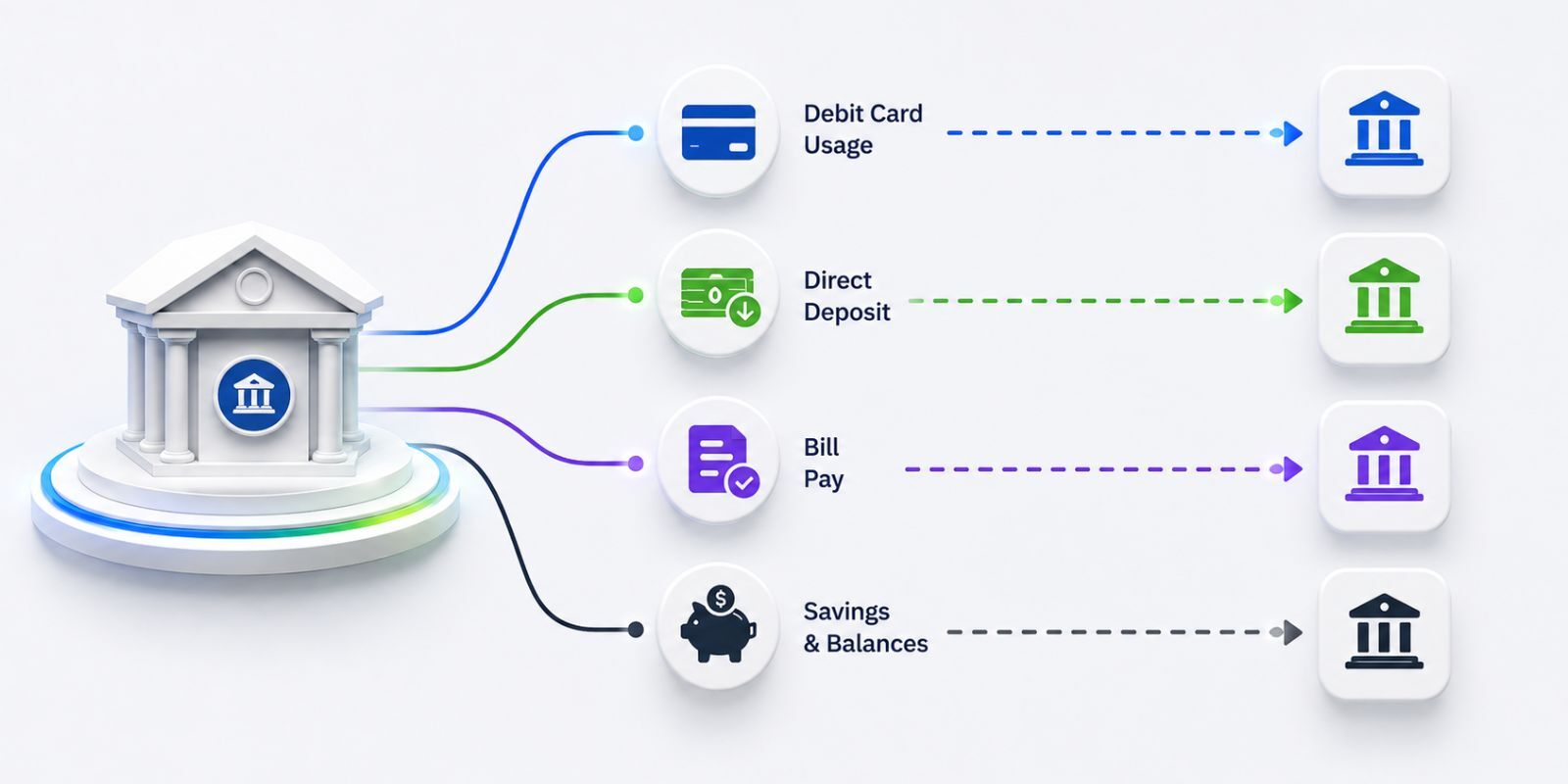

When boards ask me whether they should modernize deposit products, I try to reframe the question. Checking, savings, money markets, and CDs have...

1 min read

When boards ask me whether they should modernize deposit products, I try to reframe the question. Checking, savings, money markets, and CDs have...

1 min read

Banks and credit unions have a quiet problem. The checking account is still open and the customer or member is still on the books. From a distance,...

1 min read

At one time, Sears was unstoppable. Its name stood alongside America’s industrial greats. It built the tallest building in the world. It sold...