Joe Dugan

Joe Dugan

1 min read

A Digital De Novo Just Got a Charter. Your Efficiency Ratio Should Be Nervous.

Key Takeaways from This Blog:

1 min read

Key Takeaways from This Blog:

1 min read

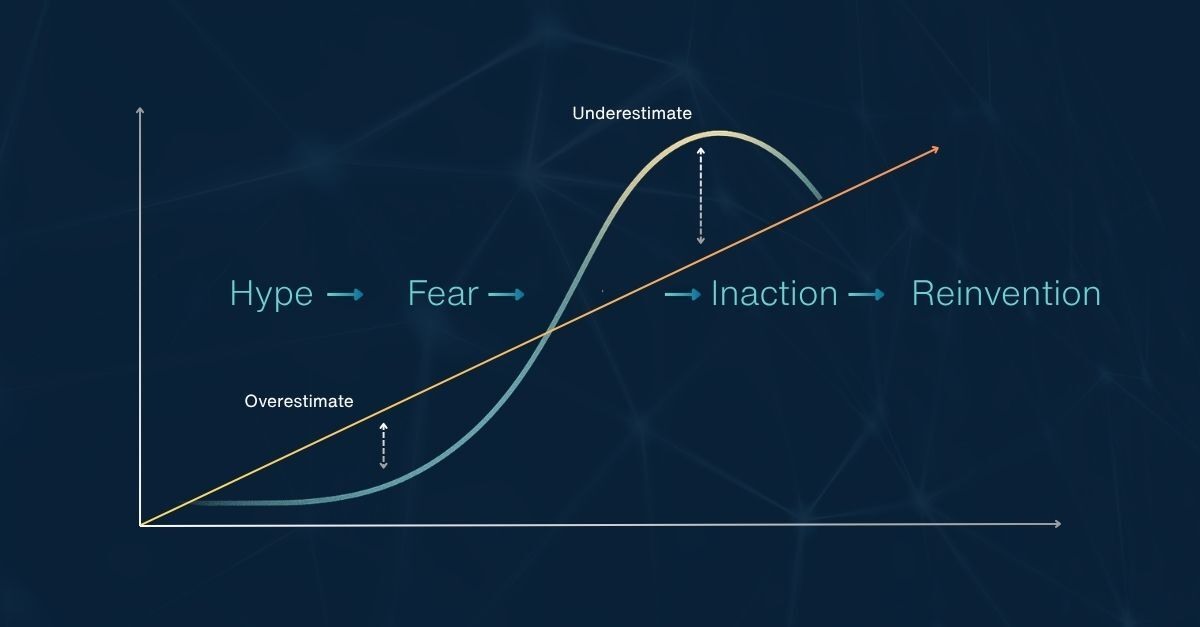

Key Takeaways From This Blog: Each wave of innovation, online banking, mobile, now AI, follows the same cycle: hype, hesitation, and eventual...

1 min read

Key Takeaways From This Blog: The Universal Banker is evolving into a digital, real-time advisor powered by AI, instant payment rails, and...