Joe Dugan

Joe Dugan

1 min read

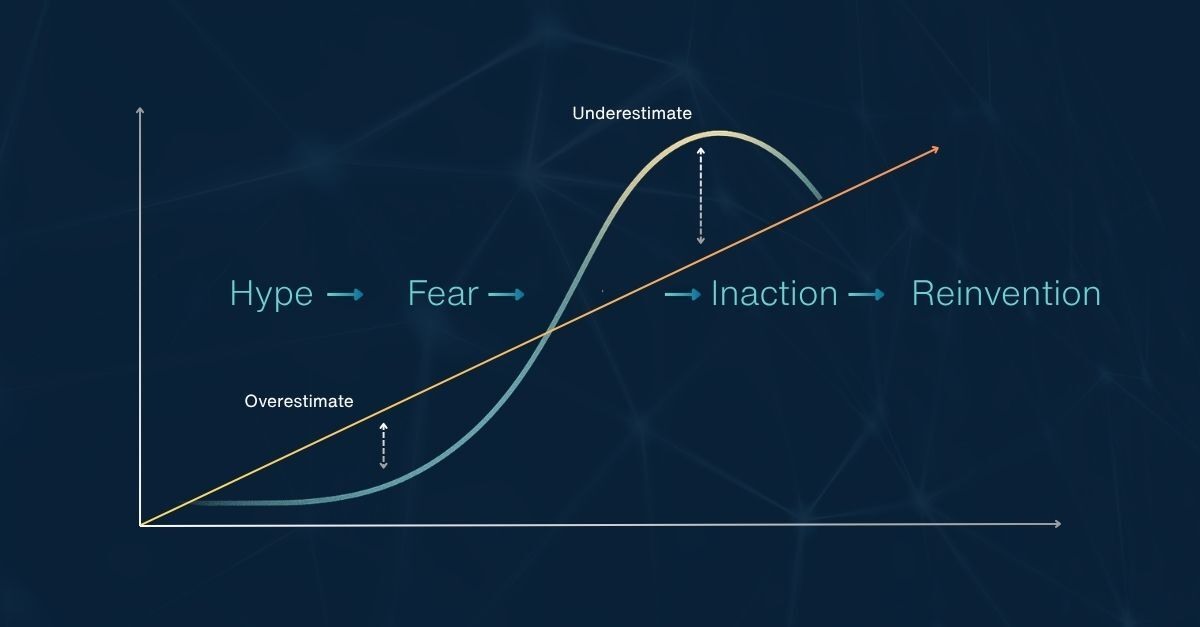

Amara’s Law and the Fear That Stalls Banking’s Future

Key Takeaways From This Blog: Each wave of innovation, online banking, mobile, now AI, follows the same cycle: hype, hesitation, and eventual...

1 min read

Key Takeaways From This Blog: Each wave of innovation, online banking, mobile, now AI, follows the same cycle: hype, hesitation, and eventual...

.jpg)

1 min read

The banking industry is experiencing a shift in how its customers conduct their financial business. When the last of the Baby Boomer generation makes...

1 min read

The mixed bag of challenges and opportunities the economy presents in the second half of 2024 is quickly becoming a catalyst for action. Conducting a...